The BIR has recently released new policies on the use of revised Income Tax Returns as found under Revenue Regulations No. 2-2014 for taxable year 2013. The annual income tax returns BIR Form Nos 1700 and 1701 for individual taxpayers have been enhanced, and BIR Form No 1702 for non-individual taxpayers has been divided and classified into three (3) categories: EX for exempt under the tax code, RT for regular income tax rates, MX for multiple income tax rates.

List of Income Tax Returns for Specific Users

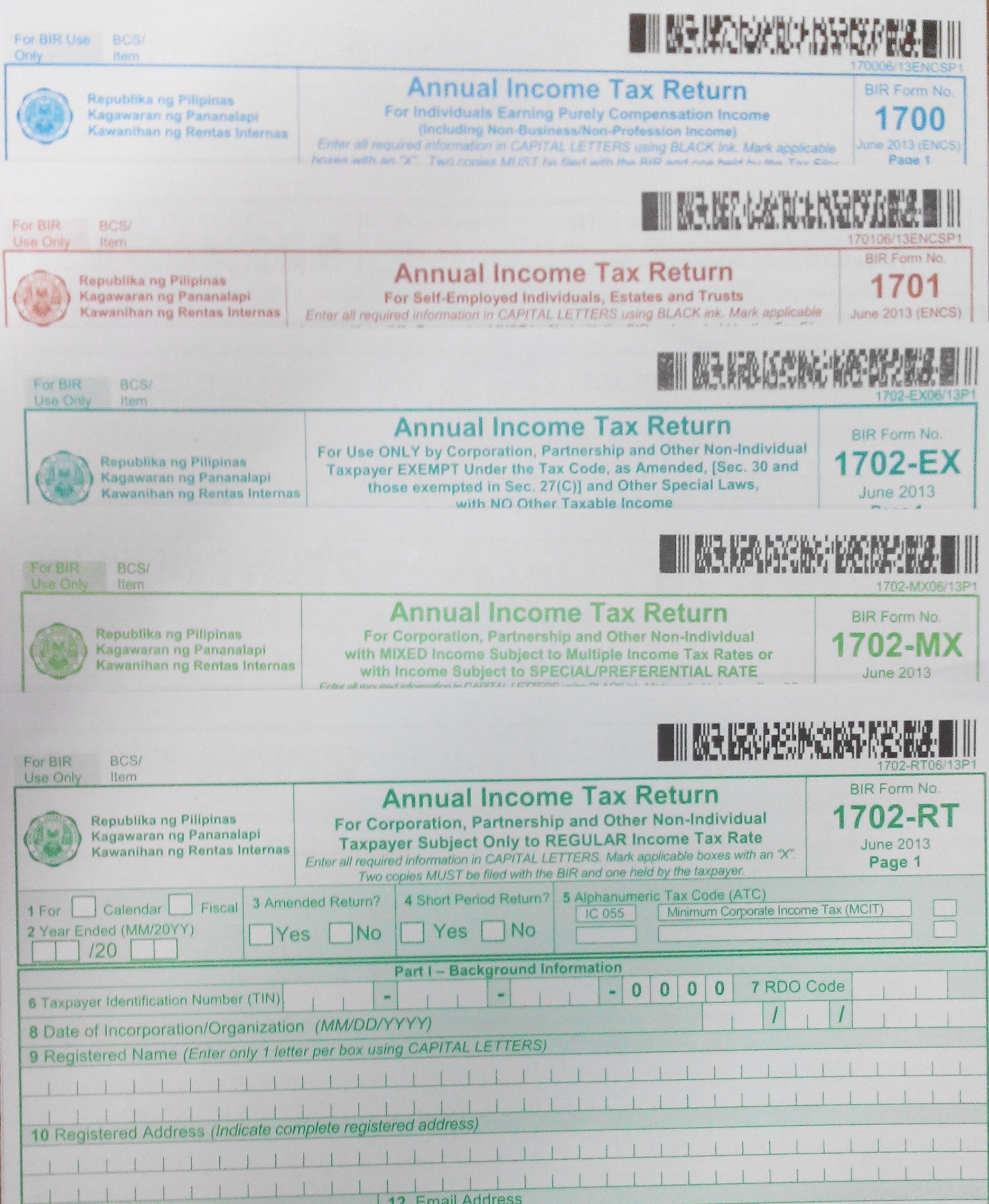

a. BIR Form No. 1700 version June 2013 – Annual Income Tax Return for Individuals Earning Purely Compensation Income (Including Non-Business/Non-Profession Income);

b. BIR Form No. 1701 version June 2013 – Annual Income Tax Return for Self-Employed Individuals, Estates and Trusts;

c. BIR Form No. 1702-RT version June 2013 – Annual Income Tax Return for Corporations, Partnerships and Other Non-Individual Taxpayers Subject Only to the Regular Income Tax Rate;

d. BIR Form No. 1702-EX version June 2013 – Annual Income Tax Return for Use Only by Corporations, Partnerships and Other Non-Individual Taxpayers Exempt under the Tax Code; and

e. BIR Form No. 1702-MX version June 2013 – Annual Income Tax Return for Corporations, Partnerships and Other Non-Individuals with Mixed Income Subject to Multiple Income Tax Rates or with Income Subject to Special/Preferential Rate)

Things to know

1. The revised BIR forms shall be used for filing of Income Tax Returns (ITRs) effective 2014 covering the taxable year ended December 31, 2013.

2. The requirement for entering centavos in the ITR has been eliminated. If the amount of centavos is 49 or less, drop down the centavos (e.g., P 100.49 = P 100.00). If the amount is 50 centavos or more, round off to the next peso (e.g., P 100.50 = P101.00).

3. Use of Mandatory itemized deductions

a. Corporations, partnerships and other non-individuals are mandated to use the itemized deductions in the following cases:

a.1 Those exempt under the Tax Code, as amended [Section 30 and those exempted under Section 27(C)] and other special laws, with no other taxable income;

a.2 Those with income subject to special/preferential tax rates; and

a.3 Those with multiple income tax rates such as income subject to the tax rate under Section 27(A) and 28(A)(1) of the Tax Code, as amended, AND also with income subject to special/preferential tax rates.

b. Individual taxpayers are likewise mandated to use the itemized deductions in the following cases:

b.1 Those exempt under the Tax Code, as amended, and other special laws with no other taxable income [e.g. Barangay Micro Business Enterprise (BMBE)];

b.2 Those with income subject to special/preferential tax rates; and

b.3 Those with multiple income tax rates such as income subject to income tax rate under Section 24 of the Tax Code, as amended, AND also with income subject to special/preferential tax rates.

In addition to the use of the manual forms mentioned (from respective links above) you can also choose to prepare, file and pay your income tax returns thru electronic means, as provided under Revenue Memorandum Circular (RMC) No. 20-2014 as follows:

1. Use of the eFPS facility

2. Use of eBIRForms Package v4.* (with Annual Income Tax Returns v2013 ENCS)

The facility and the package are accessible from the BIR website, www.bir.gov.ph. Try to browse the respective system’s Frequently Asked Questions and the respective form’s job aids packed in the package.

If you have questions and clarifications, call the BIR Contact Center at 981-8888 or email to contact_us@cctr.bir.gov.ph or post them in the message area.

____

“I wish there is a convenient tool for filing my returns and/or paying my taxes so that I can fulfill my obligation comfortably.”

~A Taxpayer’s Wish

(updated link 8/8)

Views – 4755

I hope there would be available online inquiry for retrieving tin numbers, because not all has a phone and its not easy to call BIR through mobile phones…

just saw this post. hope you can discuss how to fill up the 1701. more power!

thanks for this information.